“`html

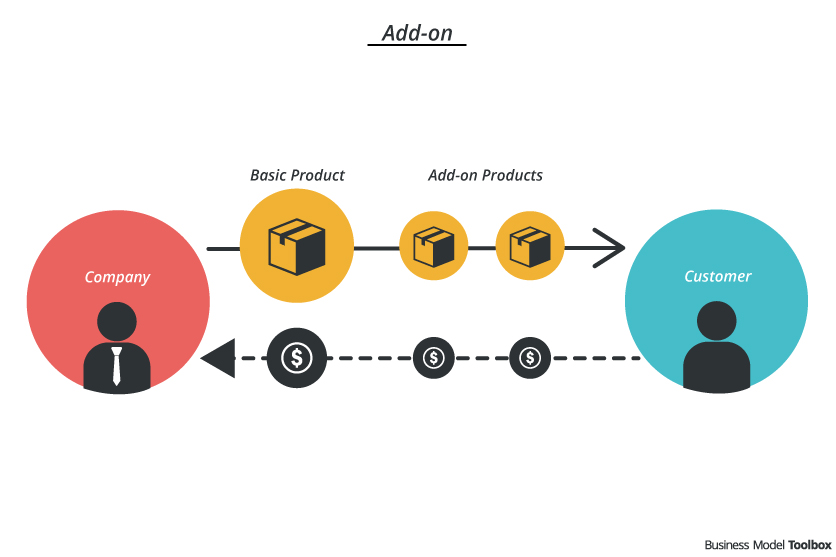

Add-on finance, also known as ancillary finance, refers to a range of financial products and services that are offered alongside a primary purchase, such as a car, a home, or a major appliance. These add-ons are designed to enhance the value of the original purchase or provide additional protection and peace of mind to the buyer. While they can be beneficial in certain situations, it’s crucial to understand what they are, how they work, and whether they genuinely offer good value for money.

Several common types of add-on finance products exist. Perhaps the most familiar is extended warranties, which extend the manufacturer’s warranty and cover repairs for a specific period after the original warranty expires. Another popular option is gap insurance (Guaranteed Asset Protection), particularly relevant for car purchases. If the vehicle is totaled or stolen and the insurance payout is less than the outstanding loan balance, gap insurance covers the difference. Credit life insurance and credit disability insurance are also common. These policies pay off the loan balance if the borrower dies or becomes disabled and unable to work.

Other add-on products include paint protection, fabric protection, tire and wheel protection, and key replacement services. These aim to protect the asset from cosmetic damage or the inconvenience of lost or damaged keys. Some dealerships also offer pre-paid maintenance plans, promising discounted rates on routine services like oil changes and tire rotations.

The appeal of add-on finance lies in its convenience. Offered at the point of sale, they are presented as a way to simplify the purchasing process and protect against unforeseen expenses. Salespeople often emphasize the potential cost savings and peace of mind that these products offer. However, consumers should approach add-on finance with caution and conduct thorough research before making a decision.

One of the main criticisms of add-on finance is that it can be overpriced. The cost of the product is often marked up significantly, and the coverage provided may overlap with existing insurance policies or warranties. For example, homeowners insurance may already cover some of the risks addressed by a specific add-on. Furthermore, the terms and conditions of these policies can be complex and restrictive, making it difficult to claim benefits when needed.

Before agreeing to any add-on finance product, carefully consider the following: Assess your needs: Do you genuinely need the extra protection or coverage offered? Compare prices: Shop around and compare the cost of the add-on with similar products from other providers. Read the fine print: Understand the terms and conditions of the policy, including any exclusions or limitations. Consider your existing coverage: Check whether your existing insurance policies already cover the risks addressed by the add-on. Negotiate: Don’t be afraid to negotiate the price of the add-on or decline it altogether. You’re not obligated to purchase it.

In conclusion, add-on finance can be a useful tool for some consumers, offering added protection and convenience. However, it’s crucial to be informed and make a rational decision based on your individual needs and circumstances. Taking the time to research, compare prices, and understand the terms and conditions can help you avoid overpaying for unnecessary coverage and ensure that you’re getting genuine value for your money.

“`

2048×1152 add finance add mexc blog from blog.mexc.com

2048×1152 add finance add mexc blog from blog.mexc.com  768×576 add acquisitions financegovcapital from finance.gov.capital

768×576 add acquisitions financegovcapital from finance.gov.capital  200×200 add finance price today add usd price marketcap chart from coinmarketcap.com

200×200 add finance price today add usd price marketcap chart from coinmarketcap.com  1601×901 add finance add lbank exchange from finance.yahoo.com

1601×901 add finance add lbank exchange from finance.yahoo.com  1972×1566 addition finance built finance solution from www.additionfinance.co

1972×1566 addition finance built finance solution from www.additionfinance.co  1200×630 add finance price add price index chart usd converter binance from www.binance.com

1200×630 add finance price add price index chart usd converter binance from www.binance.com  725×506 add interest meaning importance calculation from efinancemanagement.com

725×506 add interest meaning importance calculation from efinancemanagement.com  1280×720 advantages finance managefinancefund from managefinancefund.com

1280×720 advantages finance managefinancefund from managefinancefund.com  1620×1080 finance adnet from www4.ad.net

1620×1080 finance adnet from www4.ad.net  1140×641 add interest overview calculated implications from www.wallstreetoasis.com

1140×641 add interest overview calculated implications from www.wallstreetoasis.com  600×400 add interest definition formula cost simple interest livewell from livewell.com

600×400 add interest definition formula cost simple interest livewell from livewell.com  1920×550 finance addisons advisory group from www.addisons.net.au

1920×550 finance addisons advisory group from www.addisons.net.au  2560×1326 adpoint finance ad billing revenue accounting software lineup from lineup.com

2560×1326 adpoint finance ad billing revenue accounting software lineup from lineup.com  2397×1563 finance overview from corporatefinanceinstitute.com

2397×1563 finance overview from corporatefinanceinstitute.com  1344×1008 af finance add from www.charleskunken.com

1344×1008 af finance add from www.charleskunken.com  474×291 add synonyms add antonyms similar words add from thesaurus.plus

474×291 add synonyms add antonyms similar words add from thesaurus.plus  422×750 addition finance addition financial limited from appadvice.com

422×750 addition finance addition financial limited from appadvice.com  1200×628 add synonyms similar words phrases from www.powerthesaurus.org

1200×628 add synonyms similar words phrases from www.powerthesaurus.org  3763×4704 finance from www.on-finance.fr

3763×4704 finance from www.on-finance.fr  963×372 usains add ons adventures usain van boldt from usainvanboldt.com

963×372 usains add ons adventures usain van boldt from usainvanboldt.com  768×287 add sales definition benefits implement from www.retaildogma.com

768×287 add sales definition benefits implement from www.retaildogma.com  1200×1553 finance lecon introduction la finance definition de la from www.studocu.com

1200×1553 finance lecon introduction la finance definition de la from www.studocu.com  1200×900 add sale investors wiki from investors.wiki

1200×900 add sale investors wiki from investors.wiki  968×376 addon finance from addonfinance.com

968×376 addon finance from addonfinance.com  1024×768 addon add add helpful examples from grammarhow.com

1024×768 addon add add helpful examples from grammarhow.com  836×557 add business model toolbox from bmtoolbox.net

836×557 add business model toolbox from bmtoolbox.net  1120×320 fund extension guide finance space from www.mfsuk.com

1120×320 fund extension guide finance space from www.mfsuk.com  768×432 add synonyms related words word add from grammartop.com

768×432 add synonyms related words word add from grammartop.com