Understanding the difference between a finance lease and an operating lease is crucial for businesses acquiring assets without outright purchase. These two types of leases have distinct accounting implications and impact a company’s financial statements differently. Essentially, the classification hinges on who bears the risks and rewards of ownership.

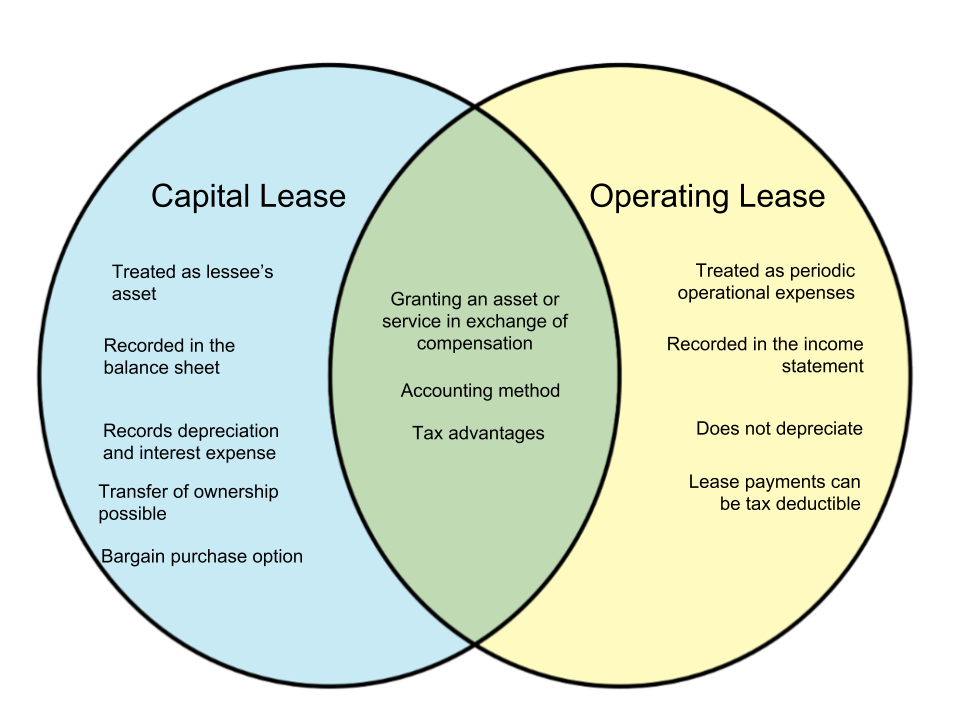

A finance lease, also known as a capital lease, is a lease agreement that effectively transfers ownership of the asset to the lessee (the user) over the lease term. Think of it as a disguised purchase financed by the lessor (the owner). Key characteristics of a finance lease include:

- Transfer of Ownership: The lease agreement explicitly transfers ownership of the asset to the lessee by the end of the lease term.

- Bargain Purchase Option: The lessee has the option to purchase the asset at a price significantly below its fair market value at the end of the lease.

- Lease Term Major Part of Asset’s Life: The lease term covers a major part of the asset’s economic life (typically 75% or more).

- Present Value Substantially Equal to Fair Value: The present value of the lease payments equals or exceeds substantially all of the asset’s fair value (typically 90% or more).

If any of these criteria are met, the lease is classified as a finance lease. The lessee records the asset on their balance sheet as if they had purchased it, along with a corresponding lease liability. The asset is then depreciated over its useful life, and the interest portion of the lease payments is expensed over the lease term. Essentially, the company treats the lease as debt financing for an asset purchase.

Conversely, an operating lease is a lease agreement that does not transfer ownership of the asset to the lessee. The lessor retains ownership and assumes the risks and rewards associated with ownership. Characteristics of an operating lease include:

- No Transfer of Ownership: There is no transfer of ownership at the end of the lease term.

- No Bargain Purchase Option: There is no bargain purchase option.

- Lease Term is Shorter: The lease term is significantly shorter than the asset’s economic life.

- Present Value is Lower: The present value of the lease payments is substantially less than the asset’s fair value.

With an operating lease, the lessee simply records lease payments as an expense on their income statement each period. The asset remains on the lessor’s balance sheet, and the lessee does not record an asset or liability related to the lease. This provides a simplified accounting treatment.

The primary difference boils down to risk and reward. Finance leases transfer most of the risks and rewards of ownership to the lessee, requiring them to capitalize the asset. Operating leases keep the risks and rewards with the lessor, allowing the lessee to treat the payments as operating expenses. Choosing between a finance lease and an operating lease depends on a company’s financial situation, tax planning, and long-term asset strategy. Recent accounting standards (ASC 842 and IFRS 16) have significantly altered the accounting treatment of operating leases, requiring companies to recognize almost all leases on their balance sheets, mitigating the historical off-balance-sheet financing advantage of operating leases.

1024×640 finance lease operating lease whats difference from www.askdifference.com

1024×640 finance lease operating lease whats difference from www.askdifference.com  750×465 understanding finance lease operating lease comprehensive from blackowlsystems.com

750×465 understanding finance lease operating lease comprehensive from blackowlsystems.com  631×214 capital lease operating lease difference comparison diffen from www.diffen.com

631×214 capital lease operating lease difference comparison diffen from www.diffen.com  1000×570 finance lease operating lease whats difference rojgarlive from rojgar.live

1000×570 finance lease operating lease whats difference rojgarlive from rojgar.live  600×252 difference finance capital lease operating lease from keydifferences.com

600×252 difference finance capital lease operating lease from keydifferences.com  410×1024 difference finance lease operating lease from differsfrom.com

410×1024 difference finance lease operating lease from differsfrom.com  550×637 finance lease difference from www.differencebetween.net

550×637 finance lease difference from www.differencebetween.net  1280×720 difference finance lease operating lease powerpoint google from www.slideteam.net

1280×720 difference finance lease operating lease powerpoint google from www.slideteam.net  1200×730 finance lease operating lease whats difference table from www.diffzy.com

1200×730 finance lease operating lease whats difference table from www.diffzy.com  960×720 difference capital lease operating lease diffwiki from diff.wiki

960×720 difference capital lease operating lease diffwiki from diff.wiki  1101×615 difference operating financial capital lease efm from efinancemanagement.com

1101×615 difference operating financial capital lease efm from efinancemanagement.com  1200×800 finance lease operating lease pros cons comparison from www.businessfinanced.co.uk

1200×800 finance lease operating lease pros cons comparison from www.businessfinanced.co.uk  768×391 finance lease operating lease darryleccain from darryleccain.blogspot.com

768×391 finance lease operating lease darryleccain from darryleccain.blogspot.com  914×500 operating lease finance lease assetz from assetz.in

914×500 operating lease finance lease assetz from assetz.in  1024×576 difference finance lease operating lease from www.superfastcpa.com

1024×576 difference finance lease operating lease from www.superfastcpa.com  955×3728 financial lease operating lease amazing comparison from www.educba.com

955×3728 financial lease operating lease amazing comparison from www.educba.com  735×411 operating finance lease debtscotlandnet from debtscotland.net

735×411 operating finance lease debtscotlandnet from debtscotland.net  768×576 financial lease operating lease key differences from www.cfajournal.org

768×576 financial lease operating lease key differences from www.cfajournal.org  1536×864 difference operating lease financial lease equipment from onlydifferences.com

1536×864 difference operating lease financial lease equipment from onlydifferences.com  800×1000 financing lease operating lease approved from www.approvedbusinessfinance.co.uk

800×1000 financing lease operating lease approved from www.approvedbusinessfinance.co.uk  1062×1074 difference lease finance ownership risk consideration from efinancemanagement.com

1062×1074 difference lease finance ownership risk consideration from efinancemanagement.com  800×3672 financial lease operating lease top differences from www.wallstreetmojo.com

800×3672 financial lease operating lease top differences from www.wallstreetmojo.com