Cheque-Based Finance in Chennai: A Declining but Persistent Practice

While digital payment methods are rapidly gaining prominence, cheque-based finance retains a niche, albeit diminishing, presence in Chennai’s financial landscape. Historically, cheques were a primary means of payment for businesses and individuals alike. Today, their usage is significantly reduced, driven by the convenience and security offered by online banking, UPI, and other electronic alternatives.

Despite the decline, several factors contribute to the continued, albeit limited, reliance on cheques in certain segments of the Chennai economy. For businesses, cheques might still be preferred for large transactions with suppliers or clients, particularly those who are not yet fully integrated into digital payment systems. Some businesses, particularly older or smaller enterprises, might find adapting to digital solutions more challenging due to infrastructure limitations, technological literacy gaps, or a preference for established practices.

Personal use of cheques is also waning. Direct deposit for salaries, online bill payments, and mobile wallets are increasingly popular. However, certain individuals, particularly senior citizens or those less comfortable with technology, may still rely on cheques for rent payments, remittances, or other routine expenses.

The cheque clearing process in Chennai operates largely through the Cheque Truncation System (CTS), implemented by the Reserve Bank of India (RBI). This system streamlines the process by capturing electronic images of cheques and transmitting them to the paying branch, rather than physically moving the paper instruments. This significantly reduces clearing time and logistical complexities, improving efficiency and security. Chennai’s robust banking infrastructure facilitates the smooth operation of the CTS system.

However, cheque-based transactions are not without their drawbacks. They are susceptible to fraud, delays in clearing, and potential loss or damage. Compared to instant digital payments, the time lag involved in cheque processing can impact cash flow management, especially for smaller businesses. Dishonoring of cheques, or “bouncing,” is also a concern, leading to legal and financial repercussions for both the issuer and the receiver. While the Negotiable Instruments Act provides legal recourse in such situations, the process can be time-consuming and costly.

Looking ahead, the future of cheque-based finance in Chennai, and indeed across India, is one of continued decline. The government’s push for a cashless economy, coupled with the proliferation of user-friendly digital payment options, is gradually rendering cheques obsolete. Banks are actively promoting digital alternatives and discouraging cheque usage through various means, such as fees for chequebooks or preferential treatment for digital transactions. While cheques are unlikely to disappear entirely in the immediate future, their role as a primary mode of payment is undoubtedly shrinking, replaced by a more efficient and technologically advanced financial ecosystem.

1200×600 essential elements characteristics cheque techy khushi medium from techykhushi.medium.com

1200×600 essential elements characteristics cheque techy khushi medium from techykhushi.medium.com  1920×816 tipos de cheques existen sus caracteristicas from rentafija.com

1920×816 tipos de cheques existen sus caracteristicas from rentafija.com  1839×976 cheques canada from www.settler.ca

1839×976 cheques canada from www.settler.ca  1200×675 computer vision object detection bank cheque from einvoice.fpt.com.vn

1200×675 computer vision object detection bank cheque from einvoice.fpt.com.vn  1200×675 cheque understanding cheque important from mybillbook.in

1200×675 cheque understanding cheque important from mybillbook.in  1600×738 cancel cheque quick guide from blog.shoonya.com

1600×738 cancel cheque quick guide from blog.shoonya.com  758×341 types cheques purposes from blog.elearnmarkets.com

758×341 types cheques purposes from blog.elearnmarkets.com  1920×845 blank bank check checkbook cheque dollars vector art from www.vecteezy.com

1920×845 blank bank check checkbook cheque dollars vector art from www.vecteezy.com  685×223 types cheque indian banking system features types from byjus.com

685×223 types cheque indian banking system features types from byjus.com  1600×900 void cheque icici bank canada cora mcclain blog from exoqbqfwy.blob.core.windows.net

1600×900 void cheque icici bank canada cora mcclain blog from exoqbqfwy.blob.core.windows.net  2360×1088 cheque types cheque parties involved cheque images from www.tpsearchtool.com

2360×1088 cheque types cheque parties involved cheque images from www.tpsearchtool.com  1000×400 cheque cheque types features key details from www.bankbazaar.com

1000×400 cheque cheque types features key details from www.bankbazaar.com  5000×3337 cheque images finder from www.aiophotoz.com

5000×3337 cheque images finder from www.aiophotoz.com  2500×1662 dishonour cheque legal recourse ipleaders from blog.ipleaders.in

2500×1662 dishonour cheque legal recourse ipleaders from blog.ipleaders.in  998×500 cheque information definition types cancelation features bank from www.bankofbaroda.in

998×500 cheque information definition types cancelation features bank from www.bankofbaroda.in  1280×720 rules cheque payments january verification from trak.in

1280×720 rules cheque payments january verification from trak.in  1024×478 write cheque india stepupmoney from stepupmoney.com

1024×478 write cheque india stepupmoney from stepupmoney.com  1024×465 cheques types cheques thesisbusiness from www.thesisbusiness.com

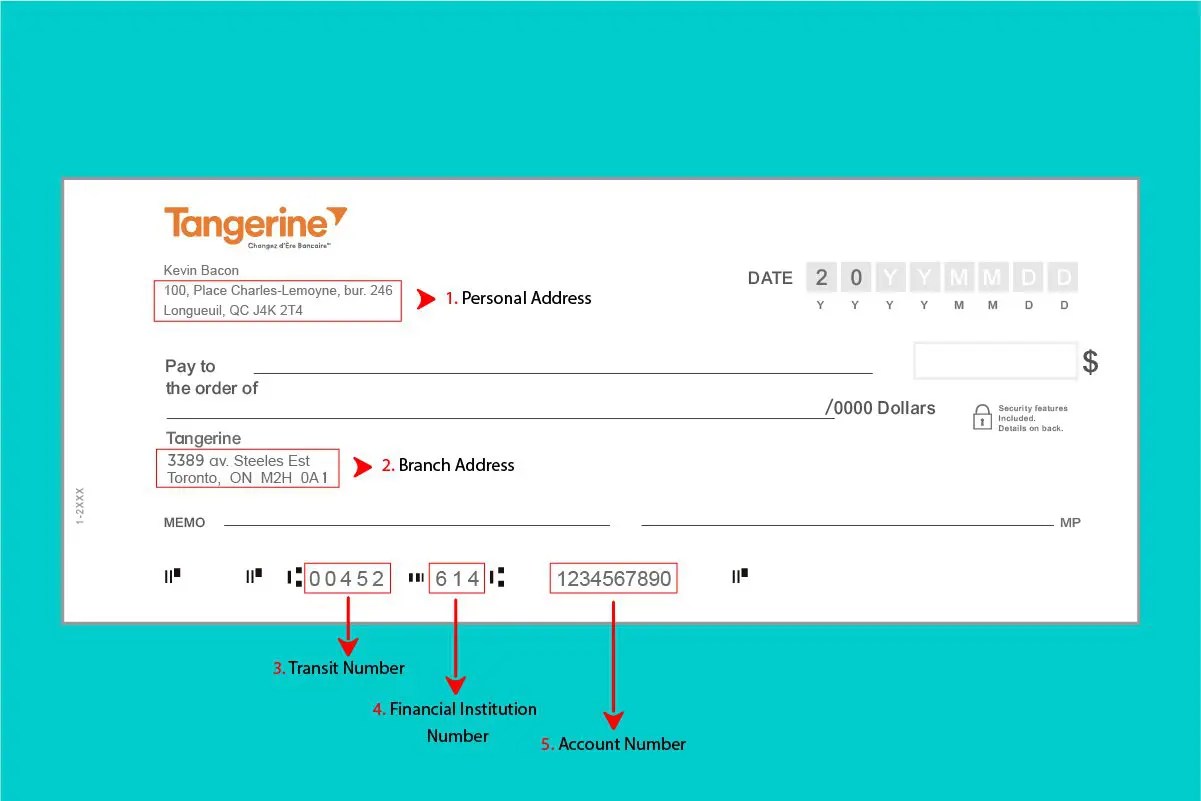

1024×465 cheques types cheques thesisbusiness from www.thesisbusiness.com  1201×801 tangerine sample cheque find from hardbacon.ca

1201×801 tangerine sample cheque find from hardbacon.ca  2400×1600 banks charge sgd cheques usage fallen from mustsharenews.com

2400×1600 banks charge sgd cheques usage fallen from mustsharenews.com  1024×466 cheque lost common che vrogueco from www.vrogue.co

1024×466 cheque lost common che vrogueco from www.vrogue.co  800×365 types cheque cheque features from testbook.com

800×365 types cheque cheque features from testbook.com  800×405 cheque meaning elements types cheque axis bank from www.axisbank.com

800×405 cheque meaning elements types cheque axis bank from www.axisbank.com  1200×667 banks making positive pay mandatory cheques issued rs from www.financialexpress.com

1200×667 banks making positive pay mandatory cheques issued rs from www.financialexpress.com  793×528 cheque cheque cheque steps filling from www.paisabazaar.com

793×528 cheque cheque cheque steps filling from www.paisabazaar.com  620×593 cheque norms write cheques correctly firstpost from www.firstpost.com

620×593 cheque norms write cheques correctly firstpost from www.firstpost.com  1020×456 gk important question bank types cheques from gkexamz.blogspot.com

1020×456 gk important question bank types cheques from gkexamz.blogspot.com  2048×937 important cheque india gepencorg from gepenc.org

2048×937 important cheque india gepencorg from gepenc.org  1117×1117 big cheque mockup print scream pte from www.printscream.com.sg

1117×1117 big cheque mockup print scream pte from www.printscream.com.sg  480×252 cheque definition types from blog.razu.com.np

480×252 cheque definition types from blog.razu.com.np  850×478 kab cheque ka pachha bha karana hata ha saina sal sa bank ja raha kaii lga bha from www.zeebiz.com

850×478 kab cheque ka pachha bha karana hata ha saina sal sa bank ja raha kaii lga bha from www.zeebiz.com  512×384 cheque definition kinds types cheques from kalyan-city.blogspot.com

512×384 cheque definition kinds types cheques from kalyan-city.blogspot.com  1280×720 types cheques india caka katana taraha ka hata ha ionetech from www.ionetech.in

1280×720 types cheques india caka katana taraha ka hata ha ionetech from www.ionetech.in